By default, the vast majority of Australians choose to invest their superannuation into “balanced funds”, because this is the default option on the application form or product selection form when they first invest with a Super fund, or begin making payments into a work related Super fund. AustralianSuper, for example, has 80% of its funds under management invested in their ‘Balanced’ fund option.

But, what exactly is a ‘Balanced’ Super fund? Definitions vary, but broadly speaking, a balanced fund is able to invest in a wide range of assets including Australian listed shares, international shares, direct property, infrastructure, private equity and fixed interest and cash. The asset allocation across these assets will vary within a broad range as defined by the asset manager.

Funds are also able to classify investments according to their own judgement. This makes it conceivable that two funds with the same potential asset mix might classify their investments and their allocation into these assets completely differently. As a result, there may be little consistency within the ‘balanced fund’ industry as to where and how your superannuation is invested.

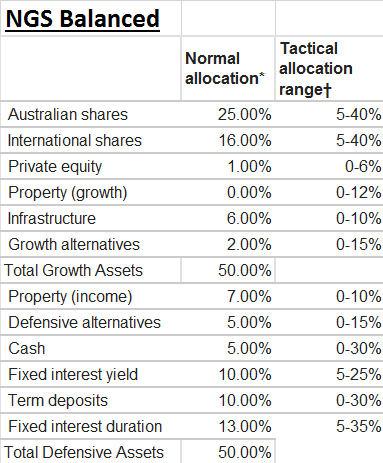

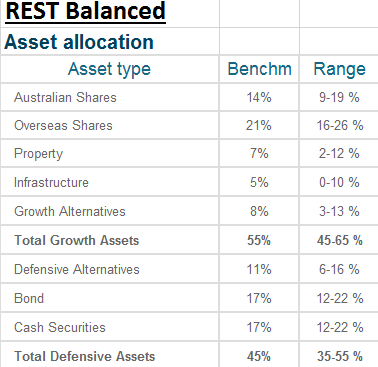

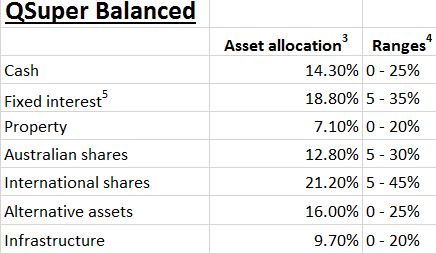

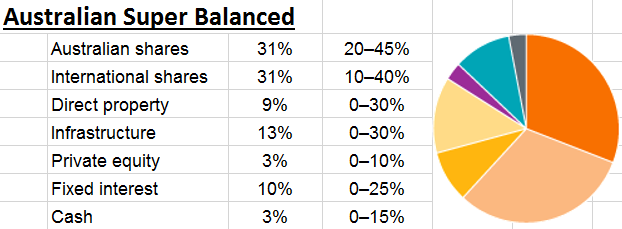

The asset mix can also change at any time at the Super fund manager’s judgement, anywhere within the broad range that they have set within their investment guidelines. The tables below show examples of these asset allocations for four ‘Balanced’ funds.

You can clearly see the wide range tolerances that the fund managers have within which they can operate. “Oils ain’t oils!” ‘Balanced’ ain’t necessarily balanced either.

The issue here is that not only can these wide ranges cause a massive difference in returns for these funds depending on the exposure they have to different asset classes in differing amounts, but how do investors know, at any point in time, what they are invested in, and what the asset mix is and whether it has changed?

QSuper & REST Balanced have 33% – 34% in cash & fixed interest compared to AustralianSuper Balanced just 13%.

A Super fund with a large exposure to US shares, say at the high end of their range at 40%, would have performed significantly better than a fund with a much smaller exposure to US shares, say at the low end of their range at 5%, over the last two or so years, because of the falling Australian dollar.

For example, AustralianSuper Balanced has nearly double the exposure that NGS Balanced has to International shares.

Can investors access this information from their ‘Balanced’ Super fund manager? And if they can, when is it available – monthly, quarterly, annually? For anyone with even a passing interest in what is happening with their retirement funds, this information is important to know as it could make a significant impact not only on short term returns but also on their superannuation funds available at retirement!

Just last week Super performance tables showed a difference of 6.1% over the last year between the #1 (12.3%) and #64 (6.2%) on the list, and both were ‘Balanced’ funds.

Over 10 years the difference between the best ‘Balanced’ at 7.6% was 3.2% compounded p.a. better than the worst ‘Balanced’ at 4.4% compounded p.a. Over many years that is potentially many hundreds of thousands of dollars difference.

The point is that undertaking this level of diligence would take hours and hours of work even if the information was freely available from the Super fund managers – which might be an interesting question to ask them!

If you need to keep checking the asset mix all the time and potentially switching between funds to achieve the ‘balance’ you determine appropriate, wouldn’t it be a much better idea to establish an SMSF and put the time and effort into managing your own money and achieving better returns? If nothing else, at least you would know where your money was invested and the asset classes you were invested in.

Perhaps something to consider…