Single ETF Strategy – with timing

Last week we discussed the use of a single ETF strategy to replicate the return of a stock market index such as the S&P500 using the SPY ETF, or the S&PASX200 using the STW ETF. This simple strategy uses no timing techniques, but is just a simple “buy and hold” strategy that aims to replicate the return of the underlying index, which also includes dividend payments.

As stated last week, such a strategy will outperform around 70% (sometimes more sometimes less for any rolling 12 month or five year period) of active fund managers in the United States and Australia, as per the research published by S&P Dow Jones SPIVA Scorecard. There is further research by Vanguard that shows that over 25 years from 1980 to 2005 that the average active mutual fund, including dividends, in the United States matched the S&P500, excluding dividends. (Source: “The Little Book of Common Sense Investing” by John Bogle, page 44).

As active investors and traders with an understanding of technical analysis tools, we can further enhance the potential returns available. Through the use of some timing techniques to enter and exit the market the aim is to be fully invested in the market during uptrends or bull markets, and waiting in cash on the sidelines during prolonged downturns or bear markets. In this way, we can take full advantage of market conditions to improve our returns over and above that of the ‘buy and hold’ method. The use of timing techniques allows us to avoid large bear markets, such as the one experienced in 2008, following the GFC, or in 2002, and to compound our overall returns by re-investing profits from previous closed positions.

In the table below, I have displayed the results of using the combination of two simple technical analysis timing techniques to enter and exit the STW ETF, as opposed to a simple buy and hold strategy, namely a customised ATR Trailing Stop and Swing peaks and troughs based on period (not percentage) swings.

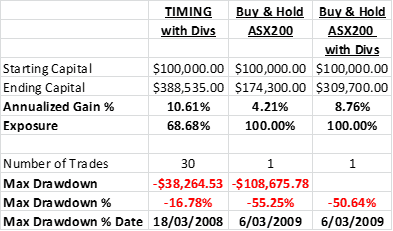

Both strategies include any dividend payments that were made during the period when trades were open. You can see that by timing our entry and exit from the STW as opposed to simply buying and holding for this 13.5 year period from Oct 2001 when the STW was first listed, would in theory, have increased our return by over $78,835, for an annualized gain of almost 10.61% compared to 8.76% for the buy and hold approach.

This immediately puts the DIY investor into the lofty realms of outperforming more than 70% of the world’s so-called professionals, the active managers of mutual and managed funds.

I have shown the returns of the spot ASX200 index in the middle column which was outperformed by 6.4% compounded per annum by the timing strategy. The spot ASX200 index, not the Accumulation (or Total Return Index in the USA), according to John Bogle in the book referenced above, is the domain of the average mutual/managed fund.

Of particular importance to us as active investors, is that we would also have suffered a significantly smaller maximum drawdown! By timing our exit from the market, at appropriate times, we would have preserved our capital and suffered much less emotional and psychological turmoil than the “buy and hold” investor by limiting drawdown to just -17% compared to a freezing-into-inaction -50%, or -55%!

This same information is displayed in the chart below. The solid blue area represents the performance of our hypothetical method using timing to enter and exit the STW ETF. The orange area displays the performance of the STW ETF without timing over the same period, excluding dividends.

Note too that over 13.5 years, just 30 trades were executed, or only 2.2 per annum! Hardly an active strategy.

The benefits of using ETFs as a foundation to one’s investment strategies are becoming clearer and clearer to DIY investors. Their low volatility, focus on a small list of instruments, asset class diversification and removal of single stock shock outcomes allow for simple investing strategies to be deployed in the market. Add some basic timing to your arsenal and the advantages over the buy and hold strategy or managing large stock portfolios is clearly evident.

The use of leverage is also open to the DIY active investor. Running the same simulations over the STW including leverage of 1.6:1, or a Loan to Value Ratio of around 60% – 62% and returns can be boosted to around 13% compounded per annum over the same period with a maximum drawdown of around -27%.

This extra 4.24%cpa outperformance over the ASX200 Accumulation equates to being over $200,000 better off, over the 13.5 years, the $100,000 would be worth approx $519,000 compared to the ASX Accumulation index growing to $320,000. Now the DIY investor is really smashing the so-called pro’s, potentially putting the DIY investor into the top 2 to 5 percentile of fund managers the world over.

Next fornight we will take a look at using a multiple ETF strategy to diversify across more than one market or ETF.

Hi Gary

Nice series on ETF trading. I’m enjoying reading it.

When you invest with the timed ETF here, how do you do position sizing? Do you enter with 100% of funds when there is a buy signal? For example, upon getting the first buy signal you enter with $100k? How about subsequent buys? Do you enter with 100%, such that if you had made some profit you might enter a trade with $120k, or if you lost money you might enter with only $80k. That is, are the values compounded?

Kind regards

Shawn

Shawn,

The strategy discussed above is just focussing on a single ETF so the idea is to invest the total amount of capital when entering a position and then to exit the entire position when an exit signal occurs.

The total proceeds from the previous trade, i.e. 100% of current capital, are then re-invested into the next position which takes advantage of the holy grail of investing, the compounding achieved through continually re-investing profits.

The buy and hold approach totally misses out on this advantage because profits are never taken.

The other massive advantage that DIY investors have over large funds is that we can exit all our funds from the market and thereby sit on the sidelines from time to time whereas large funds can’t.

BTW, in the simulation used in this article, 96% of current equity was invested into each new position. I do this in research to err on the conservative side. So returns could be driven even harder than shown above.

Regards

Gary

Gary,

Interetsing! Can you please share a bit more what this is in particular the second part: “customised ATR Trailing Stop and Swing peaks and troughs based on period (not percentage) swings”

Regards

Joern

Joern,

These are two fairly mainstream technical techniques that, in this case, have been researched for index type volatility.

Most uses of Swing charts use percentage swings, sometimes called the Zig Zag indicator. Our implementation, whilst not unique, is based on Swing highs/lows over a particular period. 2 – 63 day periods of single Swings, or combinations of multiple Swings of different periods, can be used to determine trend changes, up and down.

With the ATR Trailing Stop there are two parameters, viz. period and multiple. Theoretically the ATR adapts to different volatility but in reality it doesn’t. The trick is to match the multiple to the current volatility.

Regards

Gary

Hello Gary,

Interesting that your use of indicators differs from those used in the SPA3 system.

Could you touch on why the SIROC indicator was not adopted as part of the screening process for this methodology?

Regards,

Andrew R.

Andrew,

I first started researching an ETF system in 2009. ETF investing requires timing on indices and sectors which have different characteristics to stocks.

I tried a number of technical principles and concepts over this period including, of course, various SIROC settings. As a researcher one of the key traits that I try to espouse is to be objective about the concepts that I use. I achieve this by using various statistical ratios and outcomes to determine which system is better.

The outcomes achieved by the techniques mentioned above for the ETF System were simply better for indices and sectors than the SIROC.

BTW, the SIROC was better than all the other concepts researched and tested, besides the combination of the two mentioned above.

Regards

Gary