We may be approaching a history making event in the next few weeks so now is a good time to put this event into perspective. Whatever the outcome of the event I’m talking of, it will be analysed and investigated millions of times over in years to come.

Over the past few months, readers of this journal, viewers of the Switzer TV show on which I have discussed this content and customers that have read the Share Wealth Systems Between the Charts communique will have become familiar with my discussion about the secular bear market that equities investors have suffered the world over for around 13 years now.

To end the current secular bear market the S&P500 and Dow Jones Industrial Average need to make and confirm new all-time highs which are 1576 and 14198, respectively. The DJIA is about 2% from its all-time high and the S&P500 just under 5% away from its all-time high.

The market indices do not have to reach their respective all-time highs to retrace from there. However I do believe that a retracement right now is unlikely and that equity markets will track higher from here to test and surpass their previous all-time highs. What happens when these all-time highs are reached and even surpassed is what will be interesting.

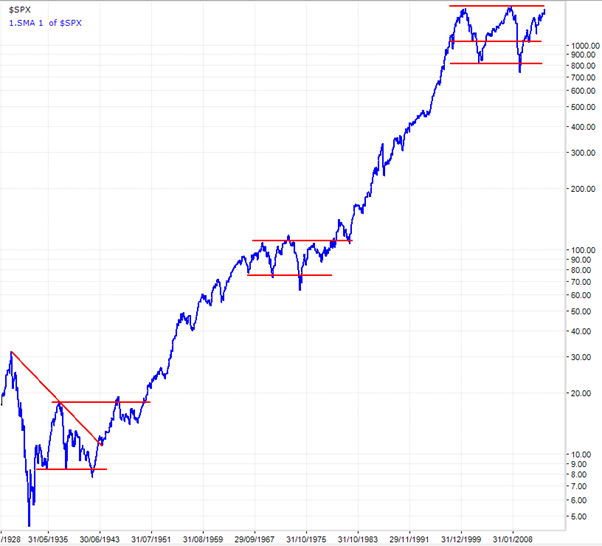

There have been other secular bear markets in the past. To help put the really big picture into perspective consider this chart of the DJIA over 116 years.

You might say that we are in the fourth secular bear market since 1896, using the DJIA. The market rises in-between the secular bear markets are secular bull markets. The existence of the current secular bear market is even clearer in a long term chart of the S&P500.

It is a trait of a secular bear market that it comprises primary bull markets that can rise by as much as 100% and primary bear markets that can fall by as much as 60%. Primary bull markets end secular bear markets when they break out of the long term range.

The event that is about to take place in the next few weeks is the testing of the upper resistance zone that defines the top of the secular bear market and potentially defines the base of an ensuing secular bull market. As you can see from the charts above there are only 3 such events in the past 116 years where the changing of the guard from a secular bear to a secular bull has occurred. We could indeed be approaching a spectacular time in world equity markets that will be analysed in the future just as we are doing right now for 1924, 1949 and 1982.

If a breakout to new highs occurs then there is bound to be a pull back to retest the previous highs. The market will need to bounce higher from there to confirm the new secular bull market or fall back into the secular bear’s grasp…..

The case against the start of a secular bull market:

- World economic problems persist with huge debt in Europe and the United States.

- This secular bear market has only lasted around 13 years whilst others have lasted 18, 20 and 17 years.

- It is a defining trait of a secular bear market that the market battles to make new highs when previous highs are reached. It was 11 October 2007 that the previous S&P500 high of 1576.87 was etched into history by the S&P500. This high slightly extended the high reached on 24 March 2000 of 1552.09. Both highs saw large retracements that followed of 55% over 17 months in 2007 and 50% over 2.5 years in 2000.

- Previous secular bear markets have ended with a primary bull market that started around the mid-point of, or slightly above, the sideways range. This would favour a serious pull back of around 30% before this secular bear market ends with a different primary bull market to the one that we enjoying right now.

The case for the beginning of a new secular bull market:

- Equity markets and world economic conditions are not currently in sync and have never been in sync.

- Bull markets have typically started during periods of low GDP growth and ended during periods of high economic growth. The western world is currently in a low GDP growth period.

- Interest rates and bond yields are relatively very low in Europe and the United States thereby pushing investors to the stock market for yield in large cap stocks.

- The contrarian indicator of money flows into / out of mutual funds in the United States supports the existence of an equities bull market.

I’m not predicting which will occur. “And quite frankly I don’t give a damn.”

The strategy that I use in the markets has long been defined. I keep investing with a medium term horizon taking long positions until I get a systematic risk exit signal to take no further entry signals and to go 100% into cash. It is quite liberating, you should try it……

Which ever happens, it may be some time before another event such as this occurs again. Be on the lookout for it.

Very interesting as always Gary. Question please. Would it be possible to resume giving your monthly short, medium and long term trend forecasts for commodities, global indices and Aussie sharemarket sectors as you used to do in the past. This was excellent reading. Thanks Gary.

I second Marks comment! Thaks Gary.

Hi Gary,

Thanks for the most interesting observation.

I would like to know what you mean by “systemic risk exit signal” as the high and low market rick indicators of SPA 3 oftern occur quite close together so how do you know when to ignore the further entry(low market risk indicator)

Much appreciated.

Very interesting – given the current global economic conditions, particularly the high debt levels. Gary, I hope you will post some more observations on this over the next few weeks. Thank you.

Response to Comments by Mick & Dale:

I will get around to doing the “Active Investor” again every now and then. I’ll use market conditions to drive ‘when’ rather than a specific time of the month.

Stopped while I had my head in research for most of the year in 2012.

Regards

Gary

Hi Gary,

Obviously umteen hours of research have gone into this and ths graphs provide compelling evidence.I would like to believe a glorious high will arrive in about 18 months,but after the shenanigans leading up to 2007 it may be too soon to see the lolly jar overflowing again with a secular bull market.However 6800+ would be nice and the exit strategy may then perhaps become very important while we wait a few more years to see off the bear.On the other hand I will be watching as you suggest and hoping that 13/14 years is enough before we head off to the races again. Cheers, Jim.

Gary

Thanks for the very interesting articles – have been sharing these with friends etc.

With respect to the end of the secular bear market, given the disparity between the US and the Aussie indices, if indeed we do see the start of a new bull market in the US, do you expect the Aust market to follow it as it so often does even though ours is more of a commodity based index.

Appreciate your comments and insights.

regards

Ray

Gary

A secondary point as my post didn’t really hit the point I was trying to make – the US is at pre-GFC highs, while our market is still midway.

Response to Comment by Justin:

SPA3 is a methodology that has a medium term horizon and hence has systematic risk (or market risk) timing that is sensitive to that horizon.

Therefore, SPA3’s systematic risk timing will be more sensitive than what is required for a longer term approach that prefers less activity. I provided an idea for longer term systematic risk timing in a blog at the beginning of February: Systematic risk management for buy & hold portfolios

Other ideas include using an ATR Trailing Stop on weekly data or a new 13 week low on weekly data or a new 3 monthly low using monthly data.

Regards

Gary

Response to Comments by Ray:

Correct, the ASX200/All Ords are way behind the US Indices if you use the top of the GFC as the ‘base’ for comparison.

However, if you use the beginning of 2000 as a ‘base’ for comparison then the ASX Indices are ahead of the US Indices and you could argue that they are catching up to the ASX Indices.

From mid March 2003, the bottom of the 2002/2003 primary bear market, the ASX and US Indices are line ball.

Regarding the ‘commodity based index’ point, there are ‘character’ differences between different stock exchanges around the world, but in general, most stocks rise in bull markets and most fall in bear markets, regardless of the ‘character’ differences.

Regards

Gary