I find myself living in two trading worlds (or cities) at the moment, one where I am totally out of the market and the other where I am fully invested! Yes, both are long equities portfolios that deploy exactly the same processes and rules.

How does this come about? I’ll start with Mark Douglas’s First Fundamental Truth: “Anything can happen!” Thinking from this perspective opens one’s mind to what’s possible, from a risk and an opportunity point of view, rather than locking on and locking out (a LOLO).

A LOLO mindset can be dangerous with most things in life but especially when it comes to investing where one has to learn to go with the flow of current opportunities according to the probabilities that they offer. But what is the “flow” at any given time? This is the 64 million dollar question. Let’s illustrate with two examples.

My personal ASX equities portfolio is currently 100% in cash following a High Market Risk signal on 31 May to cease taking any new positions and to exit open positions in the market as their respective exit signals occurred. My company’s publicly traded ASX portfolio currently has just one open position, TGG, and is 5.2% invested with the rest sitting in cash on the sidelines.

The tale is very different in my company’s publicly traded NASDAQ portfolio which is being traded with real money deposited with a USA based broker with each transaction updated at the time of execution for our customers to view and audit. This equities portfolio is currently 100% invested because, according to my processes, the equities market on the NASDAQ (and NYSE for that matter) is still in, what I term, a Low Market Risk status in the timeframe in which I observe price action in the stock market. If a systematic risk signal occurs that signals a High Market Risk – using unambiguous and well-researched criteria – then I will move to cash.

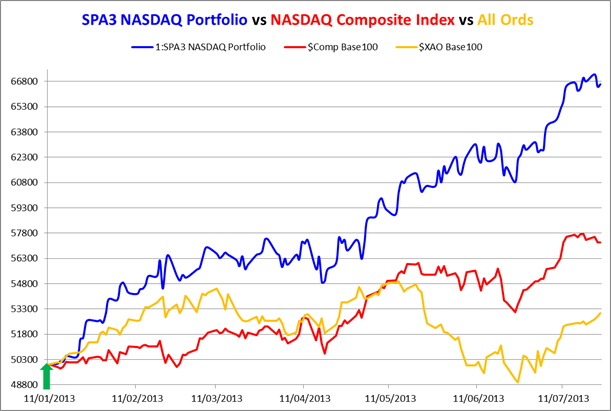

The SPA3 NASDAQ public portfolio is outperforming the NASDAQ Composite (and S&P500), and the All Ordinaries for that matter, quite handsomely at the moment excluding any adjustment for exchange rate variation. The following chart shows this.

US$50,000 was invested as at 11th January 2013 and as at 24th July the value of the portfolio was US$66,636, a rise of 33.27% (blue line) while the NASDAQ is up 14.52% (red line) and the All Ordinaries up 6.08% (orange line).

However, this is expressing all three equity curves in a mixture of currencies, the SPA3 NASDAQ portfolio and NASDAQ Composite Index in US$ (i.e. blue and red lines) and the All Ordinaries in A$.

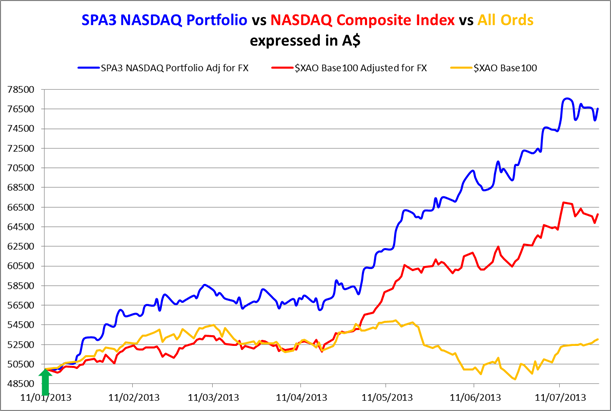

The next chart shows the performance including exchange rate variation. The currency movement has been in the favour of the US$ based portfolio over this time given that the initial investment in A$ was transferred to US$ as at 11th January 2013. The portfolio was started when the exchange rate was A$1.00 = US$1.0529 and is A$1.00 = US$0.9166 at time of writing.

Adjusted for exchange rate variation, that is, expressing all three equity curves in A$ on a daily basis, the US$50,000 invested on 11th January 2013 was worth A$76,544 as at 24th July, a rise of 53.08% while the NASDAQ is up 31.55% (in A$ terms) and the All Ordinaries is up 6.08%.

This is the Tale of Two Markets. With the proliferation of online communication, tools and platforms Australian investors these days should not only look to their domestic market to generate investment returns.

So the “flow” on the Australian market has been down to sideways since 31st May when the High Market Risk signal occurred for the ASX. But the “flow” on the NASDAQ, for my way of investing, has been “up” since 11th January and will remain so until a High Market Risk occurs on the NASDAQ Composite Index, at which time I will move my SPA3 NASDAQ portfolio to cash.

Do I know when that will happen? Absolutely not! Do I worry or fret about it? Absolutely not!

The “flow” of the market at any given time is communicated to investors via the “language of the market” which is price action. Price action occurs in multiple timeframes from price ticks to monthly bars.

The market does not communicate in innuendos, perceptions, lies, deceit, riddles or codes; the listeners of the market do all that themselves through opinions, surmise, prejudice, perceptions, biases and emotion, or what I call “noise”. If influenced by this “noise” you will suffer refraction of the “flow” causing one to suffer any one of many things, including LOLO, instead of remaining open to all possibilities.

Your task is to get into the “flow” in the timeframe that is relevant to you.

When there is a high probability of a change in flow I will have a predetermined set of simple actions that I will execute without any reservation, hesitation, fear, uncertainty or doubt. These simple actions are documented in the Trading Plan that guides my investing actions, habits, processes, routines, attitude and culture.

If you haven’t invested in this way before you should try it, it may liberate you from your current ways if they are not working for you.

Interesting that your US trading is up 33%.

I have been shadow trading for the same time and all I can do is 24% up under the selection rules I use. I think I will have to review these to find how I can do better.

A challenge for the day!

I started with $50k on the Nasdaq on 15th Jan and am up 15% in USD, but I don’t have margin so need to sit out until funds are cleared and can be reinvested. I also started a second portfolio of $50k on 15th March and that’s up 14% in USD. So at this stage both are only in-line with the Nasdaq, but well ahead in AUD!! Think I need to look into applying for some margin to stay fully invested for longer while enjoying the ride.

Hello Gary,

May I ask what asset allocation settings you are using?

Regards

Greg

Response to Comment by Greg:

The SPA3 Nasdaq Public Portfolio is using 0.9% risk per trade.

Regards

Gary