At $26.7 billion Rio Tinto (ASX: RIO) clocks in at Australia’s 11th largest listed company. RIO is also listed on the LSE and NYSE with its mining assets spread across the globe. RIO’s share price suffered enormously during the 2008 bear market falling from an adjusted high of just under $125 (pre a share split it nearly reached $160) to a low of $23.59 and has recovered around 38% of that fall.

RIO Chart

The ten year weekly chart below shows the formation of a long-term symmetrical triangle where RIO’s share price has experienced lower highs and higher lows, depicted by the black trend lines. Typically lower highs are bearish and higher lows are bullish. Which will win out? The bearish lower highs, or the bullish higher lows? Technically, when a symmetrical triangle forms, a breakout occurs when the triangle starts nearing its apex. That time is nearing and may occur any time from now to about two or so months from now.

The question is in which direction will the breakout occur? With symmetrical triangles the odds are in favor of the next directional move being in the same direction as the one in control when the triangle started forming, that is, a symmetrical triangle is typically a continuation pattern. With long-term symmetrical triangles the prior direction is not always clear, as is the case with RIO. Cases could be put forward for both but I would lean towards it having been down.

Source: Beyond Charts

Broadening our analysis to further clarify the situation, there are two major support and resistance zones that have formed over the last eight years, the two blue horizontal rectangles in the chart above. When the breakout does occur it is likely that either of these two zones will support, from below, or resist, from above, the next share price move. The next long-term directional move may only really be known when a clear breakout has occurred out of either of these two zones.

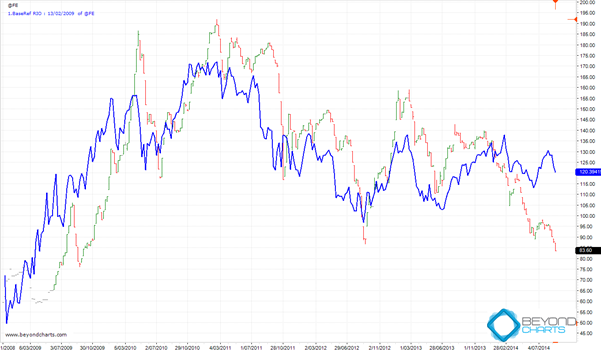

How does the Iron Ore price affect RIO’s share price?

Extending our analysis again seeking more clarification I have turned to a base comparison with the iron ore price. The weekly chart below is based from February 2009. The blue line is RIO’s share price movement and the bar chart that of the iron ore price.

Source: Beyond Charts

I’m sure that the close correlation between the two in shape and direction needs no pointing out. There is a discrepancy that exists between RIO and iron ore right now. The odds are that the RIO share price will follow the iron ore price which would mean a fall that would most probably cause RIO’s share price to breakout out on the downside. In the first chart above, this would mean a break below both the lower trend line of the symmetrical triangle and the lower blue horizontal support zone. Will RIO be able to swim against the iron ore tide or will its share price be locked into the ebb and flow of the iron ore price?

There are no guarantees in the this wonderful world of investing as there are always more variables at play than any one of us can compute at any one given time. There are only probabilities. Whilst the probabilities are for a fall in the RIO share price, any other variable could pop to the fore and have a bigger effect than those discussed above. Therefore, while RIO resolves its price oscillation, it would be prudent to wait for the next directional move to take place before deciding what action to take.

Gary Stone is the Founder and Managing Director of Share Wealth Systems.

Interesting, but what’s even more interesting is the range of interpretations that can be put on a chart. the chart you show could easily be described as an ascending triangle since early 2013 thus making the prospect of an upward breakout more likely. Secondly, with iron ore price at a 5yr low, seems more likely that iron ore won’t go down forever. Another point to note that in much of the chart I was surprised to see rio’s price pre-empt the iron ore price. On that basis it could be argued Iron ore is a about to rise, as rio is higher.

Response to Comment by Richard:

Absolutely. Viewing all the information from a chart in an objective manner is not a simple task.

What we must be very mindful of is NOT seeking patterns that only support an already formed opinion and discounting patterns and info that contravene that opinion.

We should always try to start with a neutral mindset.

I can also see a weak descending triangle from 2012.

You second point about iron ore not going lower is totally unknown at this stage. Prices can always go lower. I would rather take the view that I don’t know and I’ll let the price action tell me.

As Australian author Ivan Krastins entitled his book, “Listen to the market”, and then react.

Regards

Gary

Hi Gary

I’m being a bit naughty here. Please dont scold me too much. This comment isnt about this blog post, but rather your talk at the ATAA conference this year.

It was a very good talk that I enjoyed very much. I found myself nodding my head to the perspective points, especially in light of the punishing conditions of the Australian market over the last three years or so.

I was really interested in the latter part of the talk where you describe (dynamic?) position sizing. You mentioned an approximate sweet spot of around 0.8%. Rather than the often talked about 2%. What I am interested in knowing is how can I go about implementing this? Let’s say I have a system that breaks my trade sizes into 20 parts, so I can have a maximum of 20 open trades. That’s 5% each, although I’d have some exit strategy in place that would get me out at about 2%. How do I go about reducing that to about 0.8%? Do I just need to fiddle with the system parameters till the average loss per loss trade for the system is 0.8%? Also, you mentioned rather than using Monte Carlo you use exploratory simulation to take into account serial correlation. Could I emulate this, say in amibroker code, by using code that randomizes trades, but only randomizes them part of the time, maybe 10-20%?

I hope I havent done anything too heinous by posting this in an unrelated blog post. Sincere apologies, if so.

Kind regards

Shawn

Hi Shawn,

The dynamic position sizing aims to normalise the Loss in $ that may eventuate from each trade. It does this by adjusting the amount invested in each trade, according to a pre-defined trade risk or expected maximum loss in “%”. In this way two very different trades, one very volatile and the other very conservative, should result in the same expected loss in $ for the same amount invested. Of course the difficulty lies in defining the “expected maximum loss” and having confidence in its accuracy.

The expected maximum loss is then combined with the Portfolio Risk % to determine the position size for each trade and therefore adjusts how your portfolio reacts to losses and profits. Essentially, Portfolio Risk % is your own Master Volume(volatility) control for your portfolio.

An example:

• If you are using a simple initial stop, then the expected maximum loss in $ is known up front.

• Stock XYZ is to be purchased at $5 and the initial Stop set $0.50(10%) below. You only want to risk 0.8% of your 100k portfolio.

• The trade Value = 100k * 0.8% / 0.1% = $8000; which means you would buy 1600 shares.

• If the trade hit the stop, you would lose 1600 * $0.5 = $800 = 0.8% of your portfolio.

If you are using another type of stop that isn’t easily known at the time of entry, you will have to use your historic trades figures to determine a relationship between trade characteristics and expected maximum loss. The end equation will be the same.

You will also note that this method does not directly control the number of trades. Nor does it limit the expected share price loss by adjusting the system parameters. Money management occurs AFTER the trade rules. In my opinion money management should never dictate the trade Entry and Exit prices. So no, you don’t need to play with your system parameters in order to reduce your losses. The only time this is valid, is if the position sizes resulting from the above formula create too many small trades or only a few very large trades such that the system is not practicably tradeable.

But let’s be very clear, the Portfolio Risk % of 0.8% is not a golden rule! It is based in the outcomes of testing the SPA3 trading system with our money management. For each person and for each trading system the Portfolio Risk % will change. But what we have found is that most values are well below 2%, typically between 0.5 and 1.0%

In regards to Monte Carlo, it is a great tool for a single market with very little outside influence but it has several significant weaknesses when multiple markets, money management and extreme events are involved. This is why we use exploratory simulation (ES). Emulating ES in AmiBroker could be possible but I’m not sure how. On each bar you would need to:

• At the end of the bar

o Calculate the portfolio account values; Cash available etc based on all current and just executed trades.

o Generate all the trades for the next day and sort them randomly.

o Determine which trades can be taken based on what the account allows.

• During the next bar

o Execute the trades at the specified price.

I’m not sure what randomising part of the time would achieve? An unbiased approach would let the testing tell you when the system fails and not just when you choose it to.

Hi Sean

I appreciate the comprehensive reply!

Let me begin backwards. Thanks for the ES tip. I think you’re right. It would be quite complicated to do in Amibroker. As for randomising part of it, I dont think I explained myself very well sorry. I meant using code to ignore some of the signals part of the time to account for missed buys/sells or having too many trades to select and not enough capital or open position sizes. I think this is ok, right? Though it’s not really the same as the ES you’ve described, I think. Maybe a little similar, but not the same.

Thanks for the explanation on the dynamic position sizing. Combined with the example and calculation there, it feels alot clearer now. However, I do have one follow on question. Usually in my system testing I put in code (amibroker) for a maximum number of position sizes. Should I take out such code altogether and run the code without any maximum position size imposed and see what it produces? Would it also be prudent to run the code with a maximum position size of ONE to see how the system works?

Thanks again!

Shawn

Hi Shawn,

One of the key aspects of running ES is the ability to simulate how you would have allocated your money in a real situation. Hiding trades that actually happened on a random basis goes against this. I suspect the result would be a closer match to a subjective trading system. From a portfolio perspective, I think it would underestimate the resultant portfolio movement because large gains and losses from simultaneous investments would be reduced. One of your aims should be to take every opportunity a system provides, within the means of the account, because you don’t know which ones will be a profit or loss. Hiding trades would work against this.

Your term “maximum NUMBER of position SIZES” could mean two things but I’m guessing you mean “maximum number of open positions”. I would agree with your suggestion to remove all limits until later in the research process. A robust system usually has very few parameters and open trades could be reduced by another system change. I can’t see any value in testing a limit of 1 open trade.

Thanks again for the reply!

I understand your point about taking all the trades, but in a real trading situation this isnt always possible. There are many reasons for this – missing some while away, not having enough capital to take the trade, too many signals, etc. The idea of ignoring some trades is to simulate this real world environment. I’d hazard a guess there isnt a trader alive who has not missed a trade (or many) in say a ten year period. It happens to all of us.

Yes, sorry I meant max number of open positions. For example:

SetOption( “MaxOpenPositions”, 20 );

If you remove this option, how do you determine the number of sizes a system should use later in the process? I’m fairly sure if you dont put in the above code and how much you want for each individual size Amibroker assumes one open size and all available money allocated to it. I think the answer to my question here would be to use the calculation Sean kindly provided above, but would the expected maximum loss be accurate in backtest results that used one size with all available money allocated to it?

Howard Bandy suggests the idea of testing just one open trade. It’s something I’m having trouble getting my head around too. If you see some value in it, please let me know! Dr Bandy is no dummy, so there must be something I’m missing.

Thanks again

Shawn

Response to Comment by Shawn:

Re taking all trades: By this we don’t mean take every trade that the system produces – for a multi-position strategy this would be impossible. We mean that trades cannot be subjectively omitted if there is available capital.

Limiting the number of simultaneously open positions could skip trades even if there was available capital meaning that it would NOT be the criteria of the system filtering out a trade but a subjectively chosen open position limit. Why 20? Or 5, of 16?

As part of the research process it is important to remove such filters to allow the system’s criteria to be stress tested in their own right.

Re how do you determine the number of simultaneously open positions? I assume that this is the question.

Firstly, the ONE position size mentioned above is a percent risk per trade but each absolute $ position size would be different based on the distance to the expected exit, i.e. the stop loss price.

Secondly, the system designer doesn’t stipulate upfront what the number of open positions will be, you let the research tell you that. When we do our research we stress-test 1000’s of historical portfolio equity curves with % Risk per Trade positions sizes ranging from 0.2% to 3%. We then look at the upper and lower percentiles of Max DD, Geometric Mean and a number of metrics to determine the higher probability positions sizes to remain within ones Risk and Reward Objectives.

For each % Risk per Trade position size we can then determine how many simultaneously open positions there would be over the life of the portfolio. For example we know that 1.5% Risk per Trade averages around 7-8, 1% around 11-12, 0.8% around 14-16, 0.5% around 30 and so on. But it won’t be exact because the distance to the stop loss is not exactly the same for each trade.

Re Howard Bandy’s suggestion. There is a vast difference between trading a single market system and a portfolio system. Most books and discussions around the traps discuss single market systems, i.e. a single and separate system each for, say, the S&P500 (SPY or Futures), ASX200 (SPI or STW), QQQ, Corn, Soybeans, AUDUSD etc. With such systems you would only have one open position, per market (system), at any given time.

Although I have a system design and robustness issue with this (a separate discussion some other time), there is more written material around for single market systems than for a ‘portfolio system’ or for a ‘portfolio of systems’ each of which would trade multiple markets. This is what confuses most relatively new system designers.

If you are devising an equities system imagine having a different system for every single stock!! That is the ‘only one open trade’ mindset. A ‘portfolio system’ requires a different design, research and simulation mindset and approach.

It really depends what strategy you are devising a system for. Which markets and instruments? With or without leverage?

Regards

Gary

Hi Gary

Thanks for the reply!

That has helped clarify some things for me. (Particularly with regards to single market systems. I’ve asked a few other people, and they’ve all said the same thing. It’s reassuring to hear it again!)

You wrote “Although I have a system design and robustness issue with this (a separate discussion some other time)”. I would love to read that, if you make it a topic of one of your blog posts.

Do you recommend any good resources for portfolio system level testing?

Thanks to you and the guys on your team above for taking the time to respond.

Kind regards

Shawn

Response to Comment by Shawn:

Will do a blog on single-market system design vs multi-market system design and robustness at some stage.

Regarding portfolio system testing, most mechanical system designers simply default to using Monte Carlo simulation. In our view Monte Carlo does not stress test simulated portfolios sufficiently at the time they most need to be, during large market corrections. Monte Carlo will underestimate drawdowns for single-market systems far less than it will underestimate drawdowns for multi-market systems during large market retracements.

Re-read the 2nd last para above from Sean’s response above.

We tested a number of such simulation tools but eventually settled on one that cost US$25,000 and US$1,000 a month maintenance.

There are probably only two products that we are aware of that we believe have 1) the necessary functionality and flexibility to stress test a wide array of risk and money management variables, and 2) a simulation engine that can run 100’s of 1000’s of simulated portfolios with varying parameters with sufficient speed to complete the simulation runs within hours (2 – 24) rather than days or even weeks (one product would have been months!) for the same simulation runs.

On point 2, speed, there may be just one that is commercially available that can churn through massive simulations in a timely manner, PowerST, which we use. The other may be Mechanica.

If anybody finds any others would love to be made aware of them.

Trust that this helps.

Regards

Gary

Thanks again for the reply, Gary.

That is interesting about MC. I had a quick look at both products you mentioned, but they are beyond me both in terms of price and use. Although I’m sure with some time and application I could teach myself the necessary coding to use them. It wouldn’t be the first time I’ve taught myself a programming language. Of course the price puts them way out of my league. I suspect the price puts the products out of almost all individual retail traders league. So what do we do? I guess we default to using MC with an understanding that it’s going to underestimate DD.

Is there a quick and dirty guesstimate to account for this underestimation you have found? Say I have a system with a DD distribution between 5-10%, could I just add a possible 10% onto that to account so the DD would be 15-20%?

Kind regards

Shawn

Shawn,

You could try and account for Monte Carlo’s underestimation but you would have to do so for every drawdown period. This would prove very difficult if simulating over many years.

I can’t think of quick & dirty to circumvent the issue. The permutations mount up as the ‘re-estimated drawdown level’ will also play a role in determining the next run-up. The compounding effect, positive or negative, will be quite large.

Then there is the issue as to how you would actually build the estimation into an MC simulation.

There was another product that we tested called Portfolio Maestro which was very slow and quite complex to program to achieve exploratory simulation with its functionality, although in C# which will be well within any AmiBroker user’s expertise. There are others that are multiple 100’s of $ that use MC in various ways that may be able to be programmed to achieve an exploratory simulation outcome. Each would require investigation.

I assume that you are researching a stock portfolio system not a single-market system.

Sorry, no quick answer.

Regards

Gary

Hi Gary

Thanks again.

Hmm, well that’s a bit depressing. I’ll have a look around for some cheaper solutions and look into ES some more. Do you have any suggestions for the average individual retail trader wanting to do some system development on their own then, for this kind of MCES level testing to get an accurate picture of the system DD that we havent already discussed? I’m thinking that if ES requires such expensive, intensive software it puts system development out of the realm of average retail traders.

Kind regards

Shawn

Shawn,

The markets don’t discriminate for or against who trades them. They are neutral and are an endless stream of opportunities and risks.

Each participant, whether it be you or I or any individual investor or a multi billion dollar hedge fund have to work out a way to maximise the opportunity whilst reducing the risk, that’s it.

Both opportunity and risk will be levels that are subjective and personal but we have to find our own way or outsource. Most do the latter, usually to a managed fund of some sort.

Within finding our own way individuals have advantages and constraints, as do all other participants, albeit with different advantages and constraints.

Finding a way around the constraint you specifically mention here (I’m sure there are others that you have circumvented on your journey) will require an investment of some sort, typically time to find and/or build another path. It may require a base tool that requires additional programming.

IMHO, this sort of research should be done by all market participants. If you haven’t already, you should read The Trading Manifesto that I wrote last year. It’s a ‘white paper’ all about this subject – you can find a link to it at the top of this blog page.

I wanted to research to this sort of detail about 15 years ago and searched for tools to do so, in vain. We even tried to develop our own tools, again in vain. We only found the solution about 3 years ago.

To be honest, PC’s were not powerful enough not so long ago to do this sort of research, larger computers would have been required.

People have traded the markets for decades without such tools but the bar has definitely lifted in this area in the last few years or so.

Solving this is part of the journey. Be tenacious and find a way that fits within your constraints. When you do it will be personally rewarding.

Regards

Gary

Thanks Gary, that’s quite an encouraging message! You’re right about the nature of the markets, too. This discussion has really helped clear some confusion I’ve had regarding a few things, so thanks to you and your team for that.

I’ll take a look at the trading manifesto.

Be tenacious – will do!

Kind regards

Shawn